“Well, I’ve been ‘fraid of changin’ ‘cause I’ve built my life around you. But time makes you bolder, even children get older. And I’m gettin’ older, too.”

– Fleetwood Mac

Stepping into 2020

In 1949, George Orwell penned his ninth and final book, 1984. His famous novel describes a futuristic society filled with advanced technological tools that could be used for mass secret surveillance; Thought Police (Thinkpol) that could detect and eliminate thoughtcrime (politically unacceptable ideas and beliefs); and a Ministry of Truth that could censor and alter all information to control the past, present, and future. While this literary classic was published 70 years ago, in many respects it depicts much of the phenomena we witnessed this past decade in the 2010s. In recent years, small devices such as our phones, tablets, smartwatches, thermostats, intelligent personal assistants (Alexa), laptops, apps, smart TVs, and cars monitor what we say, what we eat, what we buy, how we sleep, our preferences, and how we live. Furthermore, while social media originally started as a medium to connect with friends online, it has exploded into an all-powerful vast reaching digital information universe capable of driving global social movements, creating instant celebrities, or ruining lives and careers in milliseconds. Additionally, the notion of #FakeNews has affected the way we receive and interpret information, with objectivity in news reporting proving to be increasingly elusive.

While the world we enter in the 2020s feels considerably different than the one we remember 10 years ago, hopefully with age comes wisdom, and with wisdom, perspective.

How did the 2010's do?

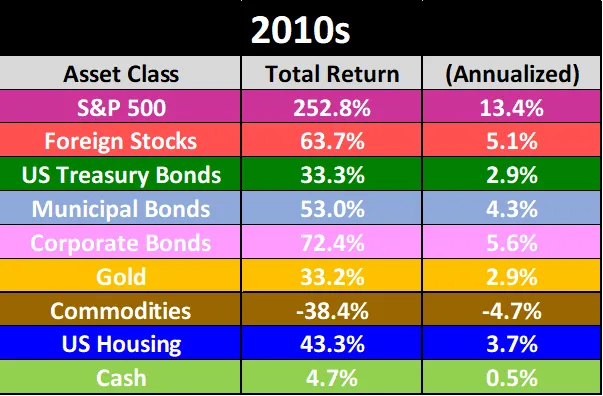

The 2010s were fantastic for US stocks, with the S&P 500 generating 253% in total returns over the decade, a standout compared to other asset classes during the same period. By contrast, the index lost 9.6% the previous decade. Commodities, which were the best performing asset class in the 2000s, fared worst in the 2010s.

This takes the current bull market for stocks out to 129 months, the longest ever on record. There are three key factors that particularly contributed to the extended run:

- Coming off a low base— the preceding 2000s were the worst decade for stocks since the 1930s, resulting from two significant recessions (Dot Com bust & Financial Crisis)

- Monetary policy— on the heels of the Financial Crisis, the Federal Reserve cut interest rates to record lows by injecting $4.5 trillion into the US economy. While the Fed started hiking again a few years ago, interest rates remain significantly lower than a decade ago.

- Corporate tax cut— the Tax Cuts and Jobs Act of 2017 marked the most significant overhaul of US corporate taxes since the 1940s, reducing corporate taxes from 35% to 21% and boosting profits for US companies across the board.

While this bull market may be the longest, it is not the strongest. The S&P 500 needs to reach 3498 to achieve that distinction, which is 8.8% above where we closed 2019.

An Unforeseen Dream

Given the headlines, this past year’s strong performance for US stocks may come as a surprise to many. Last year saw a US/China trade war, weak US manufacturing data, a global growth slowdown to the worst levels since the Financial Crisis, three straight quarters of corporate earnings declines, and a presidential impeachment.

Despite this wall of worries, in 2019 US stocks enjoyed their best yearly start in three decades; much of which was attributable to a rebound from the large selloff the prior December. The market remained buoyant through May, until a trade agreement with China was taken off the table. This development was not expected by the public and disappointed investors. These jitters were later calmed by a Federal Reserve that turned more dovish, and the central bank cut rates for the first time in a decade in July to attempt to head off a potential slowdown in the economy.

Markets started to wobble again in August over new tariffs between the US and China, signaling any potential trade deal was remote at that point. The central bank cut rates two more times in the second half of the year and stocks reacted in-kind with the S&P 500 rallying well above 3,000. Further boosting sentiment, a phase one deal between the US and China was eventually reached in December, fueling the Santa Claus rally into the year’s close. This juxtaposition of strong rate cuts whilst avoiding an economic recession provided the ideal mix for a move up in bonds and the biggest US equity rally in six years. In fact, every major asset class finished in positive territory in 2019, a rare occurrence.

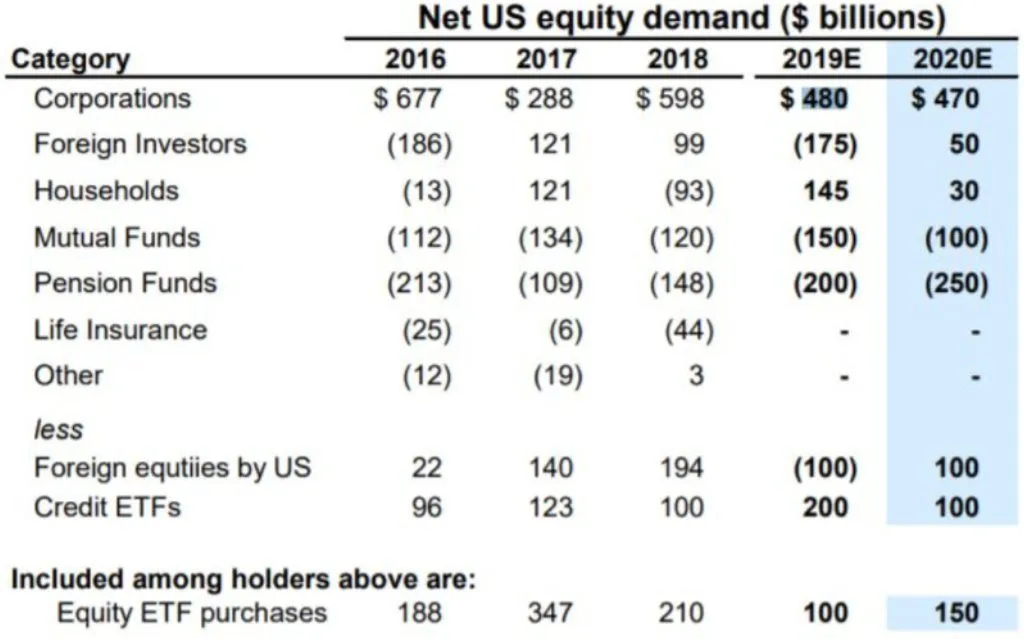

The World's Biggest Stock Investors are Betting on Themselves

By far the largest buyers of US stocks have been corporations, who snapped up nearly half a trillion dollars of their own shares in 2019. While American households also increased their equity holdings, other institutional investors such as mutual funds and pension funds as well as foreign investors scaled back their exposure to the US stock market.

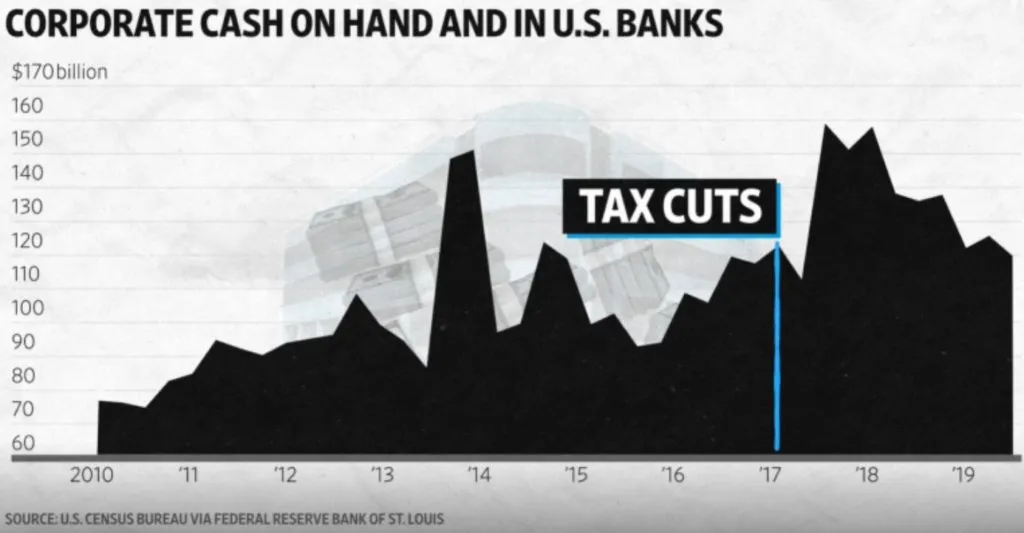

Relatively good earnings and lower corporate taxes have allowed companies to stockpile significant amounts of cash, which they have largely used to buy back shares rather than reinvest the money into their companies to fund growth. While this results in higher earnings per share (EPS) by reducing the number of outstanding shares, skeptics would prefer to see businesses put the money towards capital expenditures or research and development.

Furthermore, analysts believe the pace of share buybacks is unsustainable. In 2019, S&P 500 companies paid out more than 100% of their free cash flow in dividends and buybacks, which means that barring significantly higher earnings, share repurchases are likely to decline in the coming years.

Global Economy Down but not Out

Global growth likely slowed in 2019 to its lowest level since the Financial Crisis of 2008. The International Monetary Fund (IMF) estimates that real global GDP growth last year was 3.0%, equaling that of 2008. Advanced economies around the world grew at a 1.7% rate compared to emerging market and developing economies at a 3.9% rate. The IMF does anticipate global growth to improve in 2020 with a forecast of 3.4% this year and a 3.6% forecast for 2021. By comparison, the US (expected to have grown 2.3% in 2019) is likely to slow down in 2020 and 2021. The impact of the trade tariffs is anticipated to start becoming evident this year.

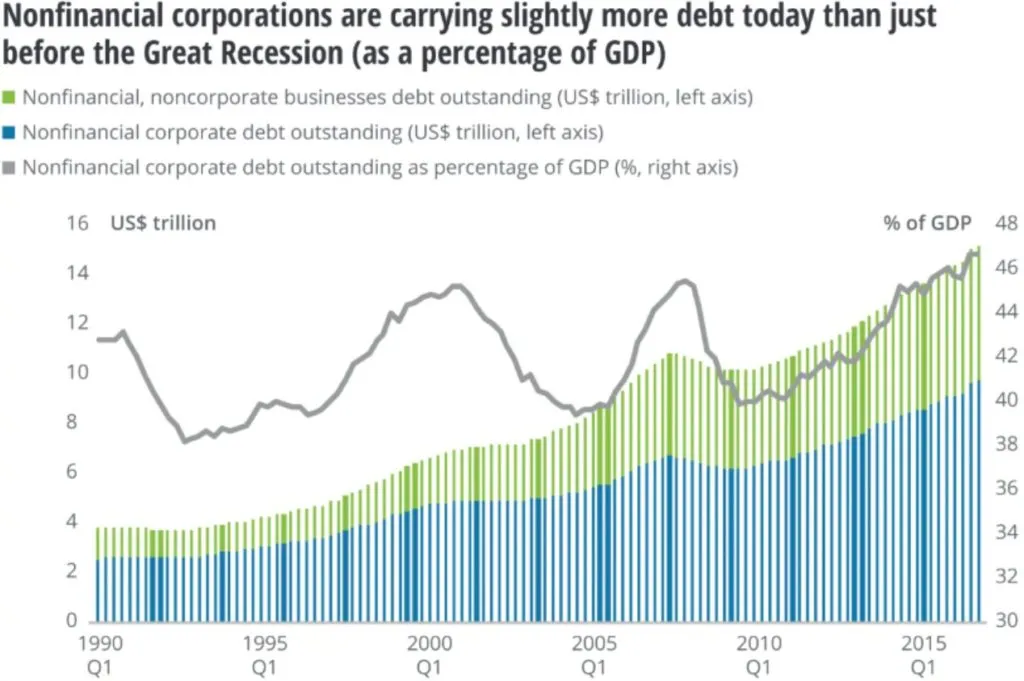

Corporate Indebtedness Highest in Decades

Low interest rates over the last decade have resulted in companies issuing record amounts of corporate debt. This fact on its own is not necessarily a concern. However, companies are also significantly more leveraged today. In fact, they are slightly more indebted today than even just before the Financial Crisis, which is a point not lost on many economists. Last May, Federal Reserve Chairman Jerome Powell made the statement, “Business debt has clearly reached a level that should give businesses and investors a reason to pause and reflect. If financial economic conditions were to deteriorate, overly indebted firms could well face severe strains. Companies holding BBB ratings (a notch just above junk) have gained special attention, but leverage has risen across all levels.

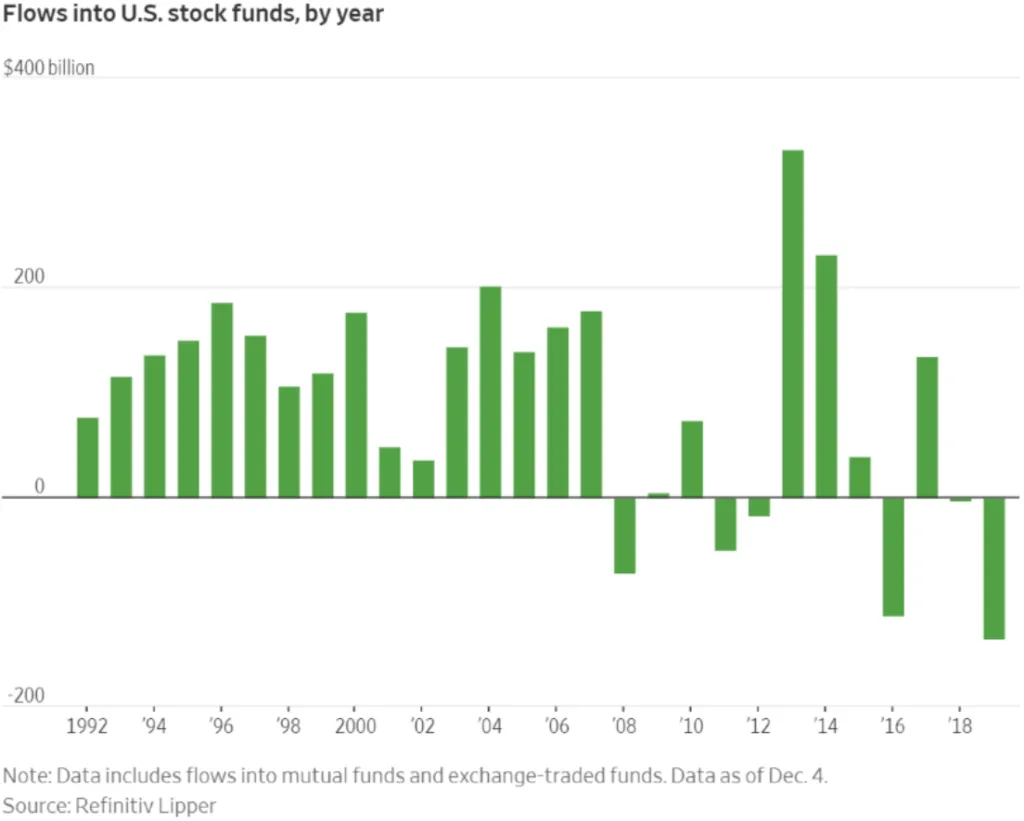

Running for Cover

With the US equity market enjoying its best year since 2013, investors pulled money out of US stock funds at the fastest pace on record. Around $220 billion was taken out of actively managed stock mutual funds in 2019, while $85 billion was put into equity ETFs, which was still an eight-year low.

Given the length of the current bull market and concerns related to global trade as well as going into an election year, investors are shifting hundreds of billions of dollars into bonds and money market funds.

Stay Cautious in 2020

Valuations have crept into expensive territory again with the forward P/E multiple on the S&P 500 back to 18.4x. This is near the levels seen at the start of 2018, which preceded a 19% correction in the stock market later that year. The higher valuation reflects lower interest rates but goes against four straight quarters of earnings declines in large US companies. While imminent risk of a recession seems less likely now than 12 months ago, this expectation is largely priced into the market already. The greater risk for investors is a contraction in valuations. This could happen if interest rates rise again if global economies are indeed bottoming out. A rise in interest rates would be particularly negative for companies that are currently very leveraged. High interest rates would compel companies to pay off debt with new equity capital, diluting shareholders and reducing earnings per share (EPS). This year, a more stable economy with a less stable market appears quite plausible.