I’ve been down this road before

And yeah I skidded but forget it.

~ Drake

Familiarity Breeds Acceptance

12 months ago the world exhaled a collective sigh of relief as it wrapped up what many viewed as the most difficult year experienced in decades. While such enthusiasm to flee 2021 may not match the sentiments of a year ago, 2021 had many unique distinctions in its own respective right. The year was characterized by political turmoil, including the capitol riot and the withdrawal from Afghanistan that resulted in the Taliban’s return to power. There was also an abundance of devastating weather catastrophes that included snow storms, floods, typhoons, cyclones, hurricanes, and wildfires across several parts of the world, serving only to intensify public concern over the prevailing climate crisis.

But there were very positive developments too. Restaurants and shops reopened their doors to enthusiastic customers, business travelers and tourists got back on airplanes, and public events were greeted with vast boisterous crowds once again.

Now as the recent Omicron variant has ignited an explosion of new cases resulting in over one million reported daily infections in the US alone (as of the first week of January), from the outside it might look like we’re back to square one; but this is not the case at all. Having become accustomed to quarantining, masking, and working and studying virtually, the emotional response to COVID in 2022 bears little resemblance to the fear, distress, and anxiety witnessed a year ago. The current proverbial “calm, cool, and collected” attitude is perhaps nowhere more self-evident than in the stock market, which has displayed great resilience in the face of an unprecedented surge of infections.

Extending the Run

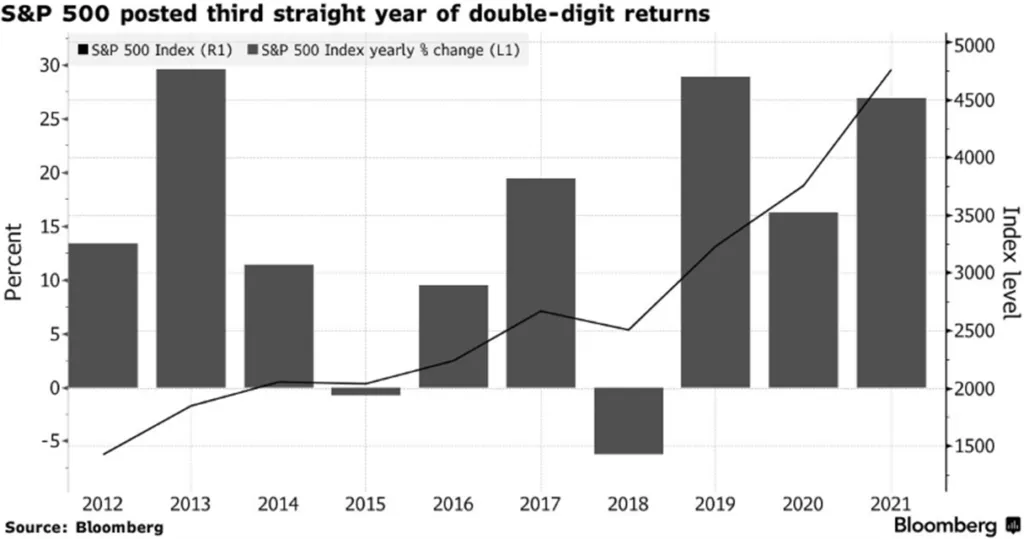

Despite coping with a pandemic that many would have hoped would be long gone by now, the stock market notched 70 new highs in 2021 and the S&P 500 rallied 27% for the year, capping the index’s best three-year run in over two decades. Even just days after the Omicron variant raged across the US, the market enjoyed its best December month since 2010.

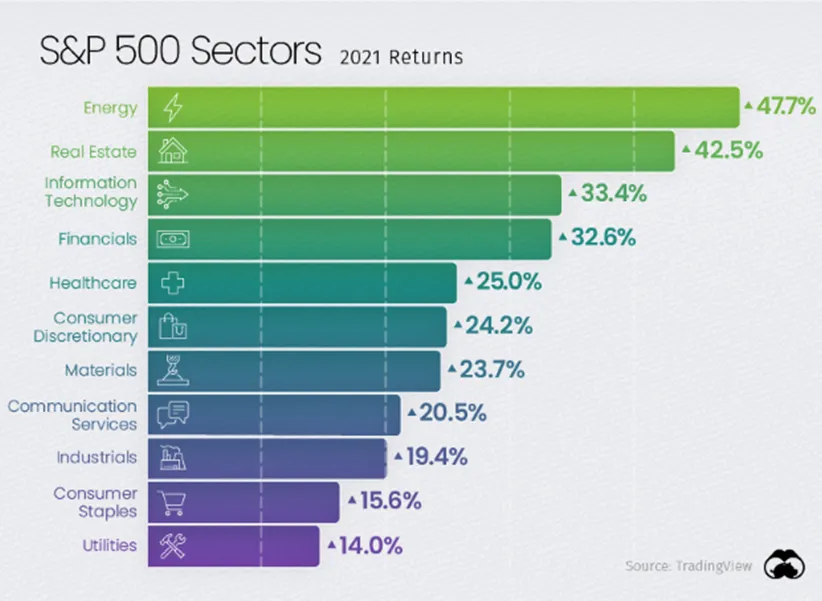

The annual rally was heavily driven by concentrated segments of the market. Goldman Sachs noted that 32.6% of the entire rally in the S&P 500 was attributable to just five companies– Apple, Microsoft, Nvidia, Tesla, and Alphabet (Google). Yet technology was not even the best performing sector last year; energy and real estate topped the index, up 48% and 43%, respectively.

Cheaper Valuations heading in 2022

Despite last year’s strong returns, however, the S&P 500 is actually trading on lower valuations today compared to a year ago. The Wall Street Journal reported that the index is trading at 21 times analysts’ projected earnings over the next 12 months, down from 22.8 times at the start of last year. The lower valuations stem from exceptional blowout earnings from America’s largest companies in 2021. S&P 500 profits rose 45% for the year, the largest increase since FactSet began tracking the data in 2008 and eclipsing the previous record of 40% set in 2010. For context, the average annual earnings growth rate for the previous ten years (2011-2020) was just 5% by comparison.

The year-over-year growth is in part flattered by weak 2020 COVID-affected earnings but is still 26% ahead of 2019, bolstered by exceptionally robust consumer demand. Companies saw net profit margins increase to a record high 12.6%, according to FactSet, and analysts project the figure to grow to 12.8% in 2022.

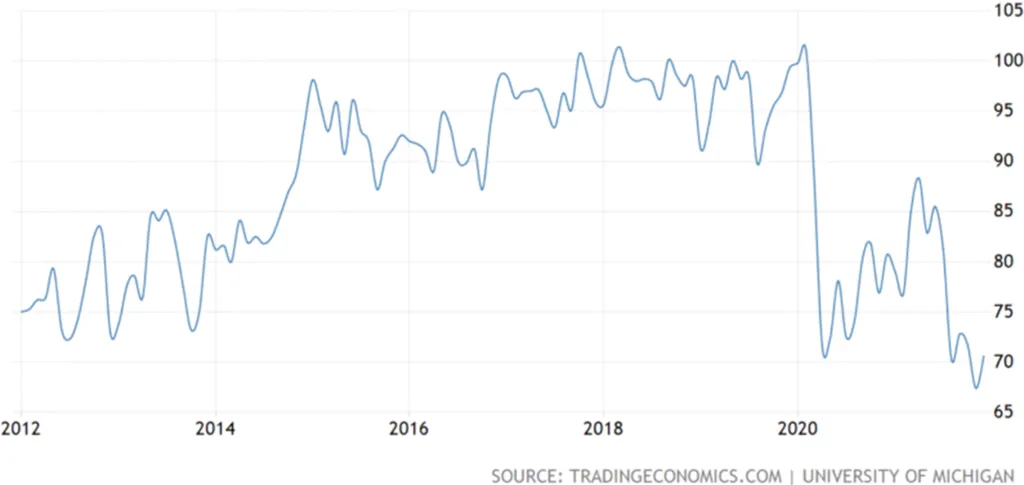

Consumers Less Optimistic Today

There is evidence, however, that consumer sentiment is starting to wane materially. As inflation has accelerated in recent months, buyers feel the higher prices diminishing their living standards and consumer sentiment dropped to its lowest level in ten years.

No Longer Transitory

The poor sentiment may come as a surprise given last year’s exceptional economic growth, plentiful jobs market, and fantastic stock performance. However, millions of American families are feeling the tangible effects of confronting higher prices on a daily basis.

After several months of maintaining that the recent rush of inflation is “transitory,” the Federal Reserve opted to leave the term out of its December meeting minutes, now acknowledging that inflation levels exceeded their expectations and that “it may become warranted to increase the federal funds rate sooner or at a faster pace than participants had earlier anticipated.” That initial rate hike may likely happen as soon as March. The market is pricing in a 67% probability of a 25bp increase at that policy meeting. In fact, two-thirds of the Fed officials are anticipating three rate hikes this calendar year, and on average, the Fed expects three more in 2023.

While the timing and frequency of the rate hikes will likely garner the bulk of the attention, equally and perhaps even more important, is the Fed’s normalization of its balance sheet, consisting of treasuries and mortgage-backed securities, which grew from about $4 trillion to nearly $9 trillion during the pandemic. Essentially, the Fed will seek to reduce its balance sheet through two means—by selling securities and/or avoiding the reinvestment of securities as they mature. The Fed’s current average weighted maturity of its securities holdings is shorter than when previous efforts were made to reduce the balance sheet (following the Global Financial Crisis), implying that it could shrink faster and also signaling the central bank’s confidence that the current economic recovery has sufficient momentum to withstand aggressive tightening measures. As the Fed withdraws its support from the bond market, yields suppressed through its quantitative easing measures will reverse course and there will be upward pressure on interest rates as investors position themselves for the Fed’s pivot on policy. Already in the first few days of this year, the 10-year treasury rate has gapped to an eight-month high and mortgage rates are back to their highest levels since the spring of 2020.

Inflation Likely to Remain Elevated

While the Fed has expressed its efforts to tighten monetary policy, there are other factors contributing to inflation that will likely keep prices elevated.

There are supply chain challenges that that will still take significant time to work out. Not enough trucks are being produced due to a global chip shortage that isn’t going away soon and there aren’t enough drivers to operate those vehicles in part due to the California AB5 law that was put into effect just weeks before COVID started. Furthermore, port blockages were a major problem, as best highlighted by the Ever Green that was stuck in the Suez Canal last March. Washington is putting in place a number of reforms, such as through the Infrastructure and Jobs Act and the Ocean Shipping Reform Act that was recently passed in December; the new legislation will take time to mitigate the existing supply chain concerns.

Additionally, inflation will continue to get pushed higher as residential leases reset and rents are driven up by higher home prices, which rose over 18% last year, according to Case Shiller. The home price appreciation has not yet been fully reflected in rents, and housing costs account for over 40% of the consumer price index.

Fed officials are aiming to reduce inflation to 2.6% by the end of 2022, compared to their current preferred price index level that rose 5.7% through November. Achieving this level of price stabilization seems ambitious and would likely require aggressive action in the face of the aforementioned inflationary forces.

2022 Poised for Growth

On the bright side, a number of economic factors point to continued growth in 2022. Analysts forecast US earnings to grow another 9.2% this year, which would well outpace the average of the previous decade. Furthermore, with demand for workers at historical highs (there were 10.6 million job openings in November), the national unemployment rate fell to 3.9%, moving below 4% for the first time since the pandemic began and is forecasted to fall to 3.5% by year end by economists. According to the Conference Board, after seeing GDP growth of what is likely to be 5.6% for 2021, they forecast the economy to expand another 3.5% in 2022, which would be quite strong relative to recent history. Wall Street firms are even more optimistic, forecasting for 3.8% growth on average. Whether such developments mean good news for investors remains to be seen, but the real economy is generally expected to be healthy this year.

Ahead of Schedule

As we enter 2022, a couple of surprising things have happened. Compared to what we might have expected 18 months ago, we remain far behind in progressing beyond the pandemic with regards to achieving endemicity or herd immunity. At the same time, our economic recovery has far exceeded even our most ambitious initial targets. This counterintuitive confluence of events means that while we remain hopeful that businesses and daily life continue to normalize, investors should be cautious as we confront the prospect of coping with the most rapid pace of monetary tightening in decades.

Given the backdrop of extraordinary returns in recent years, the considerable optimism already priced into financial markets, and the significant ramp up in retail speculation through apps and option trading, investors may want to be more modest in their target objectives this year. Coping with case surges is something we have recent familiarity with, which society is largely handling in stride. Coping with a decidedly hawkish Fed is not, and volatility is to be expected.