Deep down below the surface of the average conscience a still, small voice says to us, something is out of tune. – Carl Jung

A Few Strings Out of Place

With the S&P up significantly during the first half of the year and unemployment still hovering near historic lows, recession concerns have eased considerably since the start of 2023. Economists have raised their US Q2 GDP growth forecasts in recent weeks and home prices are turning higher after several months of declines.

Additionally, despite the Fed’s best efforts to restrict monetary policy, consumer confidence jumped to 109.7 in June from 102.5 in May, its highest level since January 2022. But while the overall picture has certainly improved, some parts of the economy continue to struggle.

For instance, despite the large rally in the S&P 500, nearly half of the sectors were down during the first half of the year. Home prices have reached new record levels in some parts of the country, but this is occurring as mortgage rates reached a new high for 2023. This is reducing new home construction and squeezing would-be homebuyers amidst already tight supply. As the cost of housing, food, health care, and transportation continues to climb, 52% of Americans now say the United States is too expensive to live in, according to a USA TODAY / Suffolk poll.

Then across the Pacific, the world’s second largest economy is not concerned about inflation at all. In China, inflation slumped to zero in June and deflation is the chief concern, along with high unemployment and mounting debt. Not everyone is basking in the recent global recovery. In fact, some are singing a very different tune.

An AI-Driven Rally

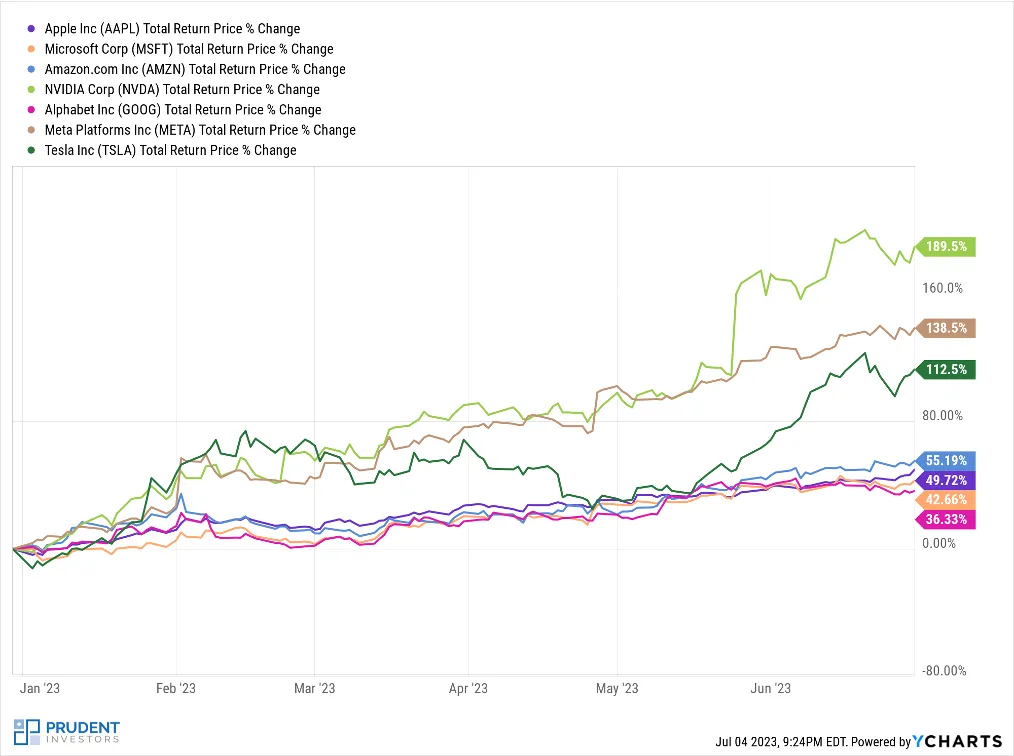

The 16% increase in the S&P 500 in the first half of the year is attributable in large part to big cap tech companies with significant exposure to AI. OpenAI’s release of its intelligent chatbot, ChatGPT, became the fastest growing software application in history. While AI has long been utilized in several applications already, ChatGPT’s creative abilities spurred the development of multiple other AI platforms and attracted massive investment.

Consequently, these seven stocks: Apple, Microsoft, Amazon, NVDIA, Alphabet, Meta, and Tesla are responsible for more than half of the S&P rally alone, exceeding the increase in the other 493 stocks combined.

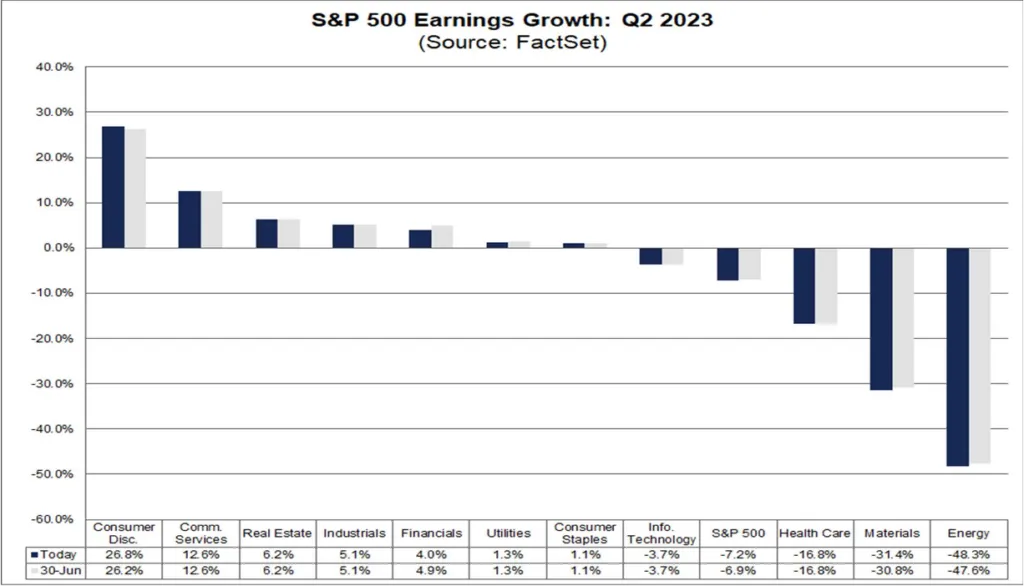

While the Technology sector flourished, several other industries declined during the first six months of the year, including Financials, Consumer Staples, Utilities, Energy, and Health Care. The highly differentiated performance is also evident across the broad stock indices.

While the Nasdaq rose 32% for its best first half since 1983, the Dow Jones rose a paltry 3.8% over the same period. The gap in performance is the largest in decades. Nevertheless, with the S&P up 24% since its October low, stocks are technically back in a bull market.

A Healthier Labor Market

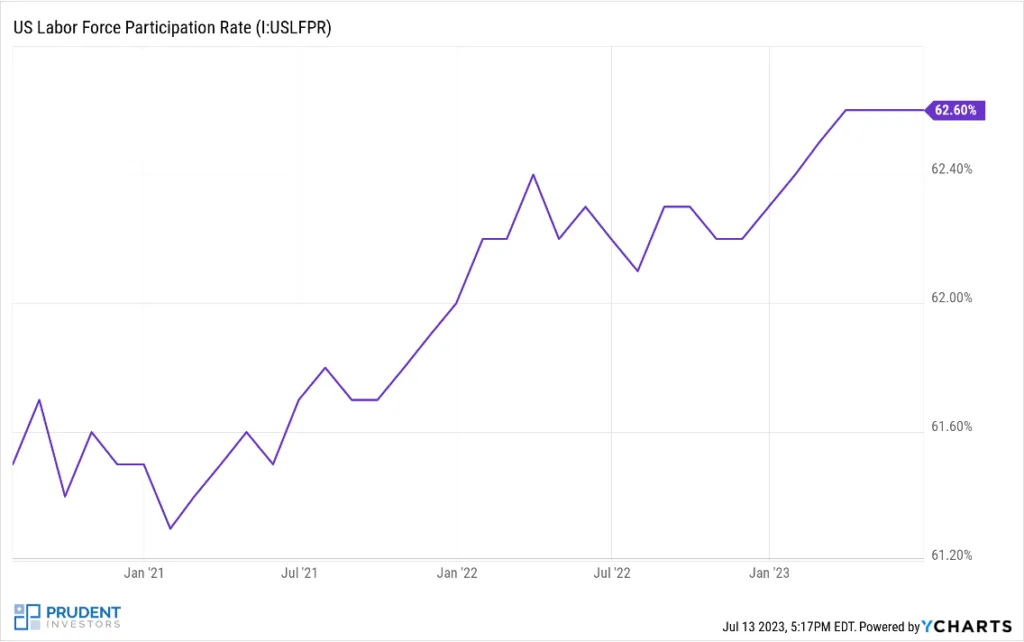

When the Federal Reserve began raising interest rates in March 2022, the national unemployment rate stood near a record-low 3.6%. Conventional wisdom at the time was that restrictive monetary policy would slow the economy and layoffs with accompanying unemployment would increase. Remarkably, following rate hikes totaling 5% over the last 16 months, unemployment still stands at 3.6% as of June 2023.

This doesn’t mean that the labor market imbalance hasn’t improved somewhat though. Two factors are contributing to better balance in recent months. First, more people are coming back to the labor force, as evident through a higher labor participation rate. This has pushed the size of the labor force from around 161 million to 167 million over the last 24 months.

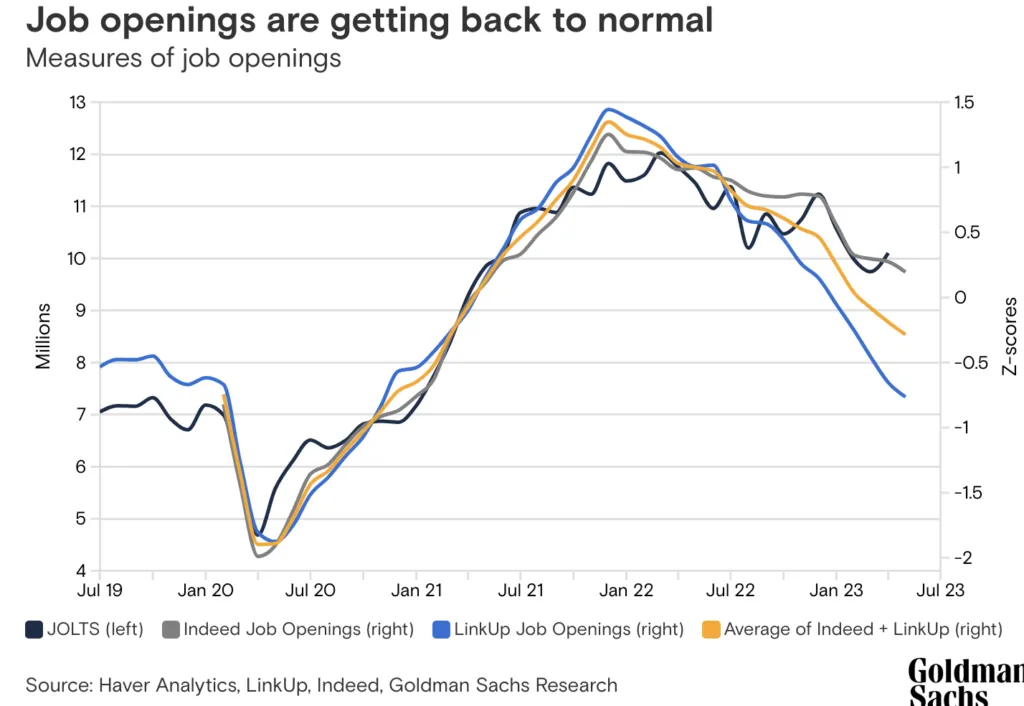

Second, job openings are falling to a more sustainable level. Although the national JOLTS (Job Openings and Labor Turnover) data only shows moderate cooling in available jobs, other metrics from LinkUp and Indeed show job vacancies are falling at a faster pace.

Economic Growth Picking Back Up

The resilient labor market has resulted in a US economy that grew roughly twice the rate the government initially forecasted and corporate earnings that well surpassed analysts’ expectations in Q1.

For Q2, the Atlanta Fed estimates the economy expanded 2.4%, which is up from its initial forecast of 1.7% at the end of April. Forecasts for the quarter have been getting pushed higher by economists across the board.

Earnings Expected to Recover in 2nd Half of 2023

With earnings season just underway, analysts estimate Q2 S&P earnings will fall over 7% compared to a year ago, which naturally begs the question, why is the S&P up 16% then? Aside from the already aforementioned AI boom, the projected profit decline is largely a function of a significant drop in forecasted earnings in the energy and materials sectors specifically. In fact, even when removing just the energy sector and measuring the rest of the market, earnings are expected to remain roughly flat.

Consumer Spending Remains Strong… in America

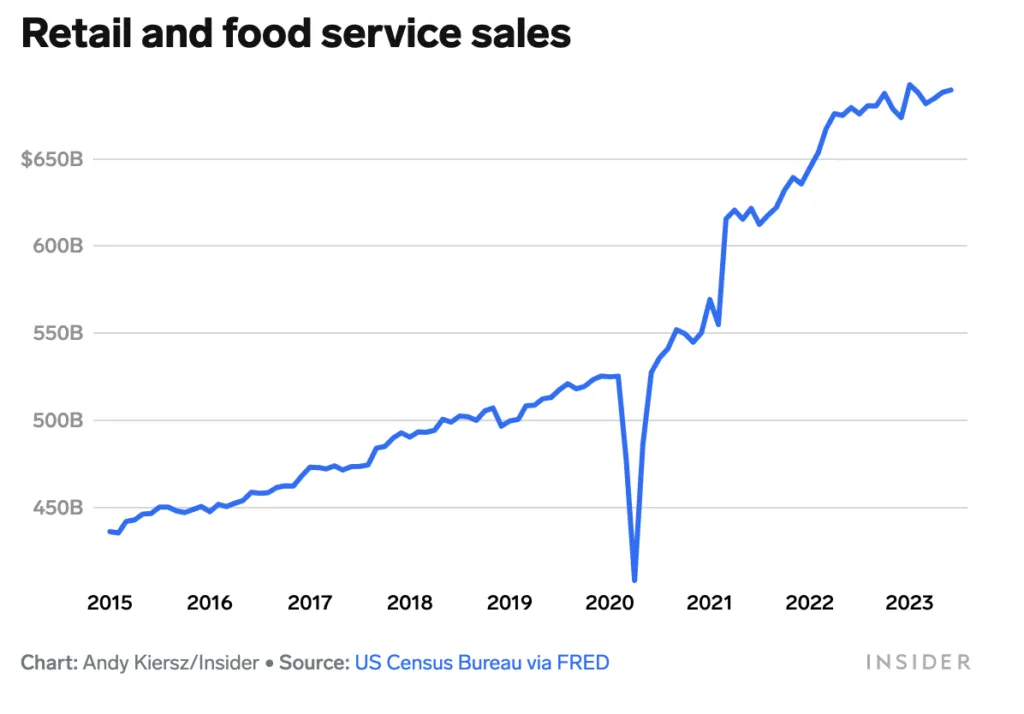

Consumer spending, which accounts for roughly 70% of the US economy, remains strong. According to the Commerce Department, shoppers and diners spent nearly $690 billion in June. US Consumer sentiment in July jumped to its highest level since September 2021 to 72.6 (far surpassing expectations of 65.5).

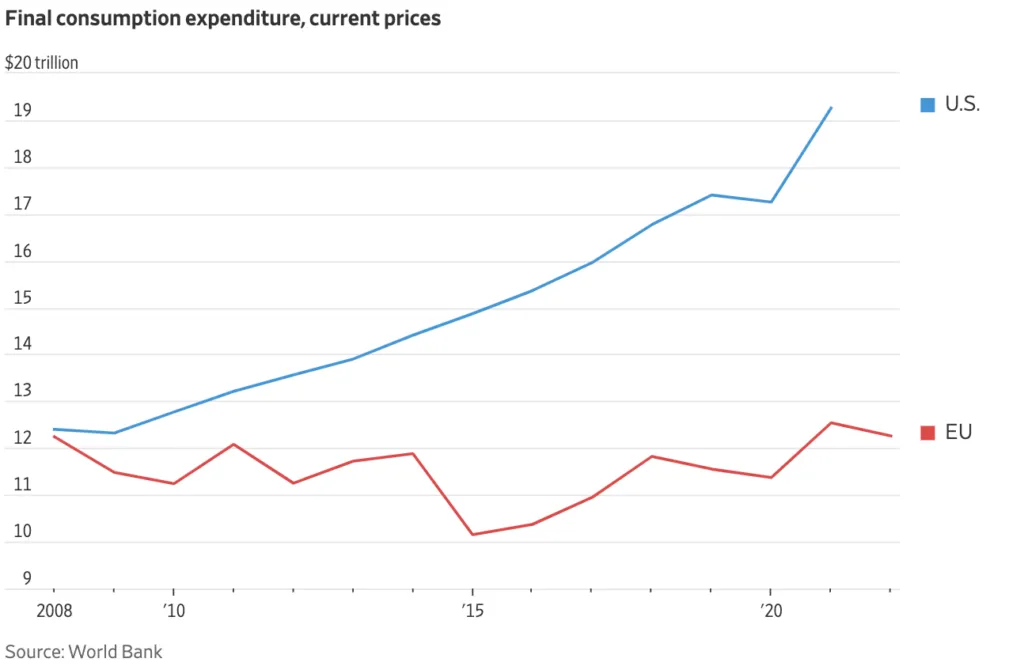

Such resilience in consumer spending has been a uniquely American phenomenon. According to the OECD (Organization for Economic Cooperation and Development), since 2019 real wages adjusted for inflation and purchasing power have declined by 3% in Germany, 3.5% in Italy and Spain, and 6% in Greece. Real wages in the U.S. have increased by 6% over the same period.

In Japan, household spending fell 4% in May from a year ago, the third straight month of declines. While base salaries grew at their fastest pace in 28 years, it still wasn’t enough to offset inflation. Real wages have fallen in Japan for 14 consecutive months.

Core Inflation Remains a Concern

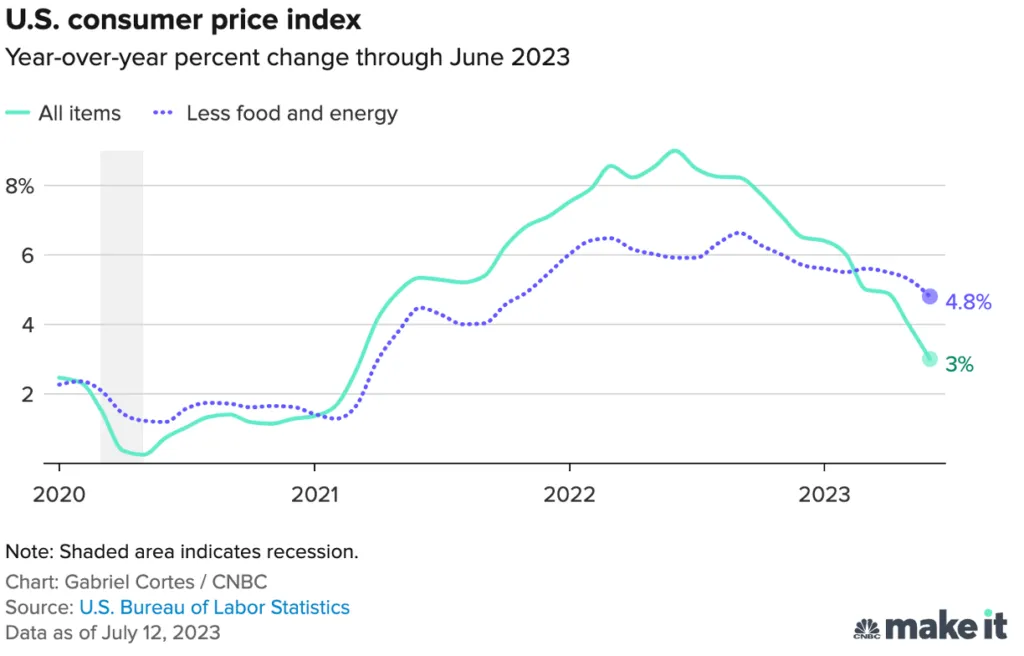

Although June’s headline inflation fell to 3% and appears to be nearing the Fed’s long-term 2% target, Fed officials remain concerned about price growth because core inflation (excluding food and energy) remains stubbornly high at 4.8% and is falling at a slower rate than they would like to see. For this reason a rate hike in July seems like a virtual certainty and the market is pricing in a roughly 1 in 4 chance of an additional rate hike in early November.

An Uneven Recovery

With growth reaccelerating, earnings bottoming out, jobs aplenty, and consumers still enthusiastically spending, the economy seems poised for a sustained recovery.

That being said, inflation continues to plague millions of households around the world as families struggle to pay higher prices for food, shelter, and other basic needs. At this point, the market has priced in much of the good news. The S&P is trading at around 19x forward earnings, which is above its 5-year and 10-year valuation averages even with a Fed Funds rate north of 5%. At this point, good news is necessary for stocks to sustain their recovery from 2022.

The repercussions of this particular rally, which is already challenging for some, may lead to some difficult questions and harsh realities in the coming days. For now, though, investors will just enjoy the rally for what it is: a far more auspicious situation than what we faced six months ago.