This frenzied period left pervasive mercury contamination from amalgamation that still exists today, depleted wildlife through polluted ecosystems and game hunting, drove vast deforestation from hydraulic mining, and altered river systems in ways that destroyed natural habitats and ruined agriculture.

At the same time, the Gold Rush also transformed California from a once-rural expanse into a state dotted with booming cities and towns. The accompanying population growth and economic boom also played a major role in the creation of America’s First Transcontinental Railroad. As it turns out, the lasting impact of the Gold Rush had little to do with gold in the end — the environmental, socioeconomic, and infrastructural effects proved far more consequential. Even with all the hysteria around gold at the time, California’s first millionaire, Samuel Brannan, was not mining for the precious bullion. He instead focused on selling the shovels, pans, and pickaxes to eager gold miners.

Today’s AI race is also changing the socioeconomic and environmental landscape. Jobs are being displaced on a massive scale, thousands of data centers are accelerating carbon emissions and straining power and water resources, AI models are trained on copyrighted works without compensating original creators, and human capital is diminishing due to an over-reliance on AI for writing and problem solving.

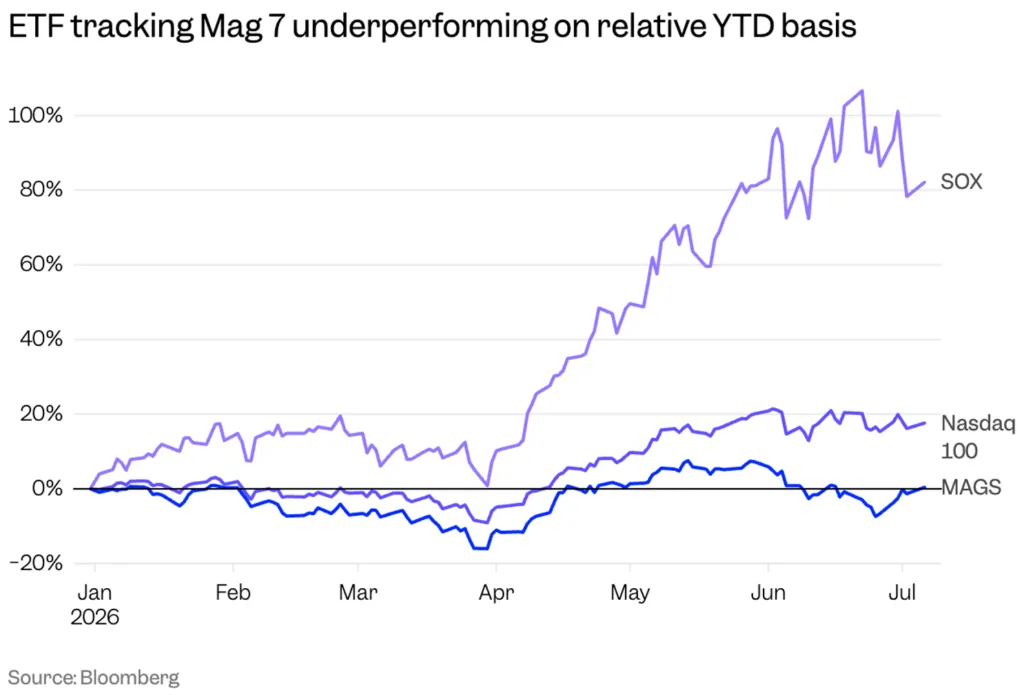

In the same breath, AI is boosting workplace productivity, advancing health care, and adding new conveniences to daily life. But as with gold, the long-term changes AI sets in motion will likely prove far more consequential than AI itself. And just as Samuel Brannan made his fortune selling picks and shovels to miners rather than mining gold himself, the real winners of the AI boom may be the chipmakers powering it rather than the AI companies built on top of it. So far this year, semiconductor stocks have significantly outpaced their hyperscaler counterparts.

In recent months, earnings are growing faster than stocks. Through July 10, the S&P 500 rose 10.7% since the start of the year. By comparison, earnings estimates rose 18.5%, which means that forward P/E multiples have contracted by nearly 8 percentage points, according to Piper Sandler.

This historic level of investment is driving a larger wedge between the haves and have-nots. According to Deutsche Bank, the top decile of listed companies by market value now account for more than three-quarters of the total corporate market capitalization in America – the highest share in a century.

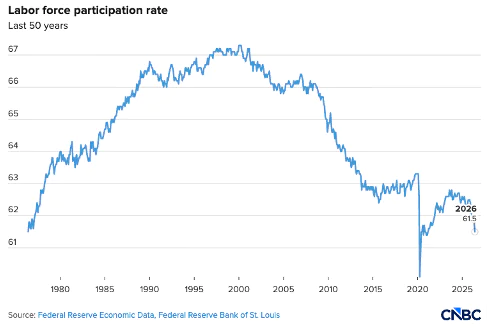

Individuals who have been looking for work for 27 weeks or more, classified as long-term unemployed, are making up a rising share of the unemployed population. Consequently, rising pessimism toward finding work is causing dejected jobseekers to eventually drop out of the labor force, which in part explains the low participation rate. The low participation rate also helps reduce the unemployment rate, which doesn’t include individuals who have stopped trying to find work.

Of the nearly two million people who have been out of work for more than half a year, those between their mid-20s to mid-30s make up the largest share. The 55+ cohort, by comparison, saw its participation rate fall to a 21-year low of 37.1%, which indicates that this group is the most likely to choose to be excluded from the labor force.

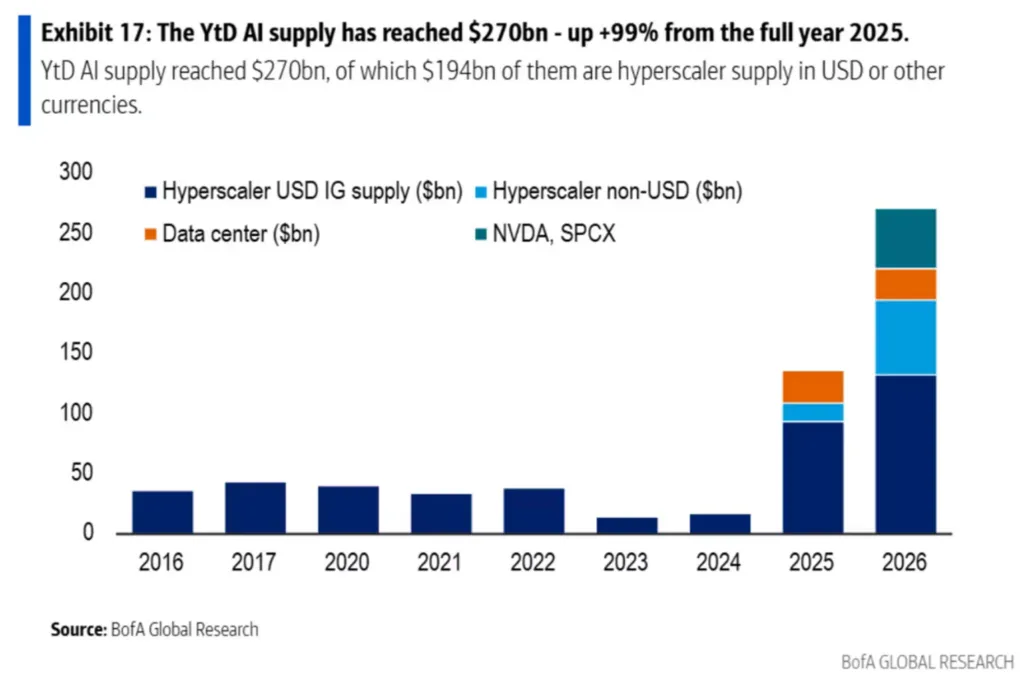

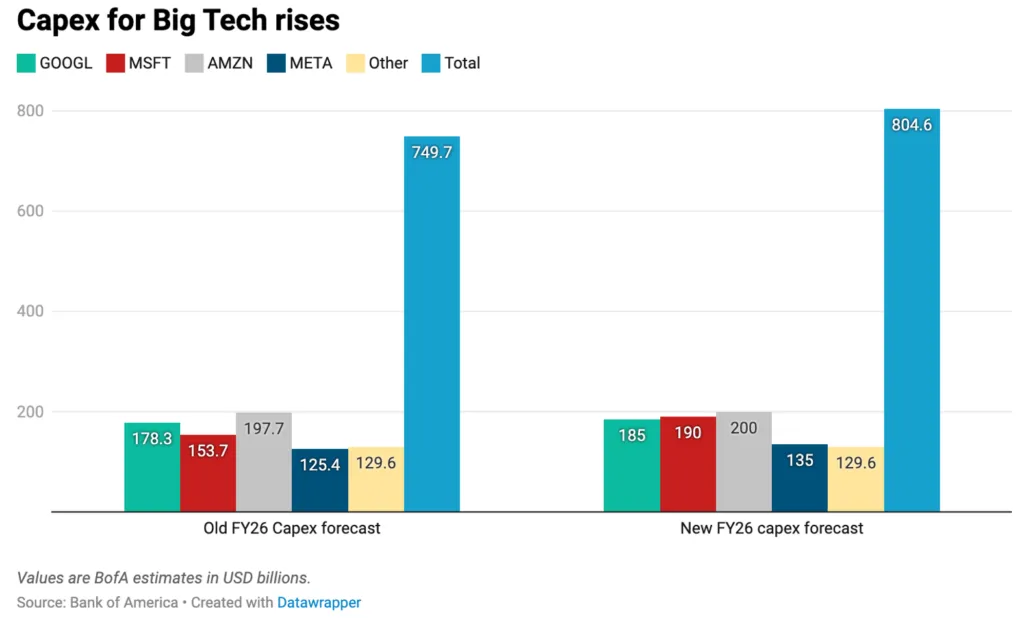

Such ambitious targets cannot be met through regular profits or cost-cutting. Companies are increasingly turning to the capital markets. Already in 2026, AI-related corporate debt has increased 99% from a year ago to $270 billion. Bank of America and Goldman Sachs forecast $2.1 trillion of investment grade debt supply this year, which would rival 2020 pandemic levels when the federal funds rate was near zero. Despite the myriad of high-profile equity offerings and IPOs this year, the bulk of the AI financing is expected to come through the corporate debt market.