It is not uncommon for a fiduciary who is marshaling assets to find one or more annuity statements. In fact, according to Wink, Inc.’s 2021 Annuity Sales Report, most annuity purchases fall between the age of 60-69. Annuities themselves can be complicated products, which is why federal entities and state governments have issued various bulletins, like this bulletin from the SEC and this bulletin from the state of Minnesota, in an effort to inform investors and protect their interests.

Many times the fiduciary is the one trying to pick up the pieces by figuring out what the annuity is, how to get needed funds out, and if there are any fees. With that in mind, here is a simplified overview of the things to look for when reviewing an annuity statement.

Contract Issue Date

When the annuity was purchased, if it can be refunded, and if there are surrender charges.

This is one of the first things that a fiduciary should look for, as it represents when the annuity was purchased by the annuity holder. If an annuity was purchased within the last few years, there may be surrender charges before the annuity can be liquidated without penalty. If the annuity was purchased very recently, it is possible that the annuity is still within the free look period. If the free look has not expired, the annuity can be returned for a full refund.

States have different rules for the length of the free look period, but in California, it is 30 days for seniors.

Fixed vs Variable

Investment risk taken by the annuity.

A fiduciary should determine whether the annuity is fixed or variable, as this can help determine the investment risk the annuity is taking. A fixed annuity is safer because it guarantees a specified return for a period of time.

On the other hand, a variable annuity can fluctuate with the stock or bond markets based on the underlying holdings within which are similar to mutual funds or ETFs. To determine whether an annuity is fixed or variable, the fiduciary should review the statement, which will show what product was purchased.

Surrender Value

How much the annuity is worth if liquidated.

Oftentimes a fiduciary needs funds from an annuity in order to fund large expenses. The surrender value represents how much the insurance company will pay out if the annuity is completely liquidated. The surrender value will represent the value minus any surrender charges or expenses.

Surrender charges vary depending on the insurance company, but some penalties for early withdrawal typically may begin at 6% to 7% the first year and then decline one percent each year thereafter.

Death Benefit

How much the annuity is worth if the annuitant passes away.

The death benefit represents the value of the annuity that is to be paid out as a life insurance death benefit if the annuity holder passed away. The death benefit and surrender benefit are often the same, but can differ depending on what riders (i.e., essentially added features to the contract) the annuity has.

Statements normally do not disclose who the death beneficiaries of the annuity are, so it is important for the fiduciary to call the insurance company to determine who is listed. Notably, if the death benefit has not been assigned and ends up being paid to the estate, then the benefits will need to go through probate in order to be distributed.

Amount Withdrawn

How much has been withdrawn.

Reviewing the amount that’s been withdrawn on the annuity statement can help the fiduciary identify if the annuity holder is using the annuity for investment growth (e.g. no withdrawals), or is withdrawing funds from the annuity for income. This provides insight into whether payments are being paid out by the insurance company. The fiduciary should then be confirming that amounts are being deposited into bank accounts.

Guaranteed Withdrawal Annual Amount

How much guaranteed income can be withdrawn.

Annuities are often purchased because of the promise of reduced risk or guaranteed income. It is important for a fiduciary to determine if an annuity is providing ongoing income for the annuity holder.

Some annuities have an amount on the statement that references a guaranteed withdrawal amount. This amount represents the guaranteed amount that the annuity holder may take per year for the rest of his or her life. However, if the annuity holder withdraws more than that amount in a year, then the future guaranteed withdrawal amounts may be decreased, or even eliminated.

Oftentimes guaranteed withdrawal amounts appear to be an amazing deal, but once inflation is taken into account it becomes apparent that guaranteed income might not go as far as expected.

Qualified vs Non Qualified

How annuity withdrawals are to be taxed.

A fiduciary should also understand the tax implications of withdrawals or liquidations of an annuity. Taxation will depend on whether the annuity is qualified or non-qualified. This information can normally be found on the first page of the statement, but if the statement does not identify whether it’s qualified or non-qualified, then it’s recommended to to call the insurance company to confirm.

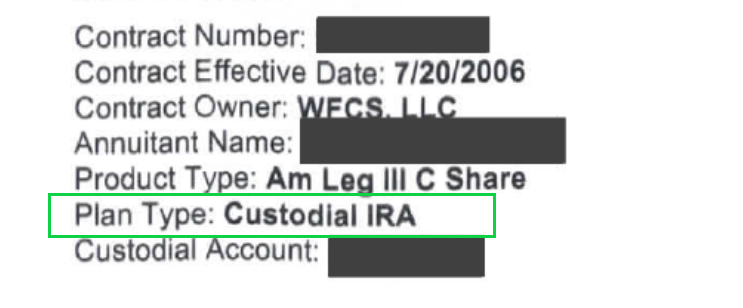

Example (Qualified Annuity):

An annuity is considered “qualified” if it is held in a retirement account and is funded with pre-tax dollars. Sometimes the only way to identify if an annuity is qualified is whether the plan type represents retirement related accounts (e.g. IRA, 401K, 403B).

Annuities that are qualified are allowed to grow tax free; and taxation occurs when funds are distributed from the annuity. Qualified annuities are normally the easiest for a fiduciary to deal with, as investments in the annuity can be liquidated without incurring a tax hit. Gains from growth are not taxed because the annuity is held within a qualified retirement account. And it is only distributions taken from the qualified annuity that are taxed at the account holder’s ordinary income rates.

Qualified annuities are subject to the same required minimum distribution rules as retirement accounts (e.g. 401I, IRA, 403bs), so if the annuity holder is over 73, it’s important to check if distributions are being taken. If not, the IRS charges a 25% penalty on any delayed or untaken distributions.

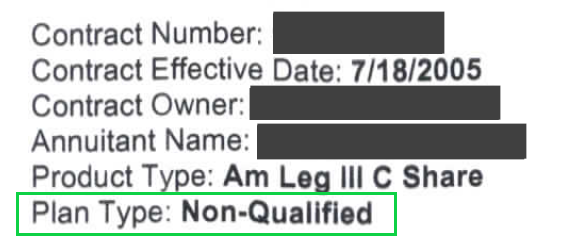

Example (Non Qualified Annuity):

Non-qualified annuities are annuities that were funded with post-tax dollars. The taxation of non-qualified annuities can be more complicated than qualified annuities. This is because unlike qualified annuities, which are only taxed as ordinary income on distributions, non-qualified annuities can create a large tax hit when surrendered. This is because the IRS taxes non-qualified annuities on any gains from when the contract was purchased. Sometimes a fiduciary is caught between a rock and a hard place when liquidating a non-qualified annuity, and the funds needed to pay for sudden large expenses end up generating a substantial tax hit.

Fees

How much is being paid in fees.

One area that is not usually very transparent on a statement is the underlying fees of the annuity. Annuities have mortality and expense fees related to life insurance. They might have fees for income riders, such as a guaranteed lifetime withdrawal benefit. And, for variable annuities, there might be fees of the underlying investments. All these fees can add up, but they will probably only be revealed through assistance of an investment advisor or by calling the insurance company.

When making decisions with what to do with an annuity, a fiduciary has many considerations. By looking at key parts of an annuity statement, the fiduciary should get a general idea of how the annuity is being used. Sometimes an annuity is being used for consistent income and sometimes it’s being used for growth. As the fiduciaries decide how to use the funds in the annuity to fund expenses, they will also need to consider tax issues.

Even though this blog attempts to distill the basic important information a fiduciary should be looking for, annuities are complex products and there is not a one-size-fits-all scenario when working with them. That’s why it’s important that a fiduciary review annuities with a trusted financial advisor. If you are a fiduciary and need assistance reviewing the annuity statement, Prudent Investors is happy to help. Contact us anytime or book a meeting with a member of our team.

This blog is general communication being provided for informational purposes only. This information is in no way a solicitation or offer to sell securities or investment advisory services. It is educational in nature and not to be taken as advice or a recommendation for any specific investment product or investment strategy. This does not contain sufficient information to support an investment decision. Any investment or investment strategy mentioned may not be suitable for all investors or in their best interest. Statistical information, quotes, charts, references to articles or any other quoted statement or statements regarding market or other financial information is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. All rights are reserved. No part of this blog including text, graphics, et al, may be reproduced or copied in any format, electronic, print, et al, without written consent from Prudent Investors. Prudent Investors does not provide legal or tax advice. Please consult with your investment advisor, attorney or tax professional before making any investment decisions. Investment advice offered through Prudent investors Network, Inc., an SEC registered investment adviser.