“Every now and then it helps to be a little deaf”

– Ruth Bader Ginsburg

On March 4, 1933, Franklin D. Roosevelt was sworn in as the 32nd President of the United States, following a landslide election victory over Herbert Hoover the previous year. The prevailing mood hanging over the country was one of deep uncertainty and dread. The last four years had been marred by a stock market crash, bank failures, record unemployment, and a ballooning government deficit. Addressing the economic crisis, FDR delivered his famous 1,883-word inaugural address to the country and immortalized the phrase, “The only thing we have to fear is fear itself.” Just weeks later, the United States gross national product fell to its lowest level for the quarter, dropping 45% from peak to trough, and unemployment climbed to 25%. Later that year, however, the economy finally bottomed out and inflation turned slightly positive while GDP growth slowly resumed that summer. In 1933, the Dow Jones enjoyed its best year in American history, rallying 64% by December 31.

While this pandemic-fueled economic crisis is vastly different from the one referenced to 90 years ago, there are lessons that can be learned. The current economic crisis saw unemployment peak in April and GDP bottomed out at the end of June. While uncertainty does indeed lie ahead in the coming months and years, investors who did not allow themselves to be overcome with fear were rewarded. By September end, the S&P 500 rose 50% from its March lows. Unfortunately, many missed the rebound. In the past, legendary Fidelity investor, Peter Lynch, was quoted to say, “Far more money has been lost by investors preparing for corrections than has been lost in corrections themselves.” As we mourn the passing of Justice Ruth Bader Ginsburg and celebrate her life and legacy, her words, “Every now and then it helps to be a little deaf,” may serve as a helpful reminder.

Increasing Odds of Democratic Sweep

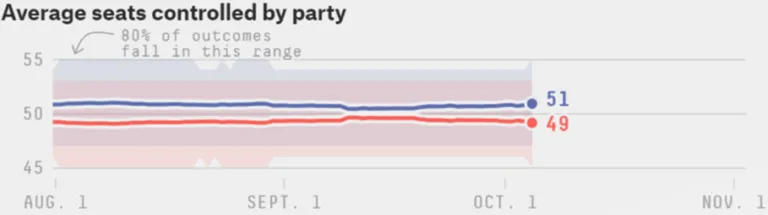

The last week of September saw odds rise for a Democratic sweep in November. Currently, most online betting and quantitative analysis websites put the probability of a Biden White House victory between 65 to 80%. The outlook for Congress, however, is mixed. While the Democrats retaining the House seems fairly certain, the race for the Senate is much closer. The Republicans, who gained the majority of the Senate seats in 2014, successfully defended their majority in 2016 and 2018. With 33 Class 2 seats up for election this year as well as two special elections in Arizona and Georgia, a total of 35 seats are up for grabs. Of those 35 seats, 23 are opening up from the Republican Party and 12 from the Democratic Party. According to data analysis group, FiveThirtyEight, the Democrats have a 66% chance of taking control of the Senate this Fall; taking an average of 51 seats in their simulated outcomes.

Forecasted Senate. Source: FiveThirtyEight

Blue Wave: Higher Taxes and Bigger Stimulus

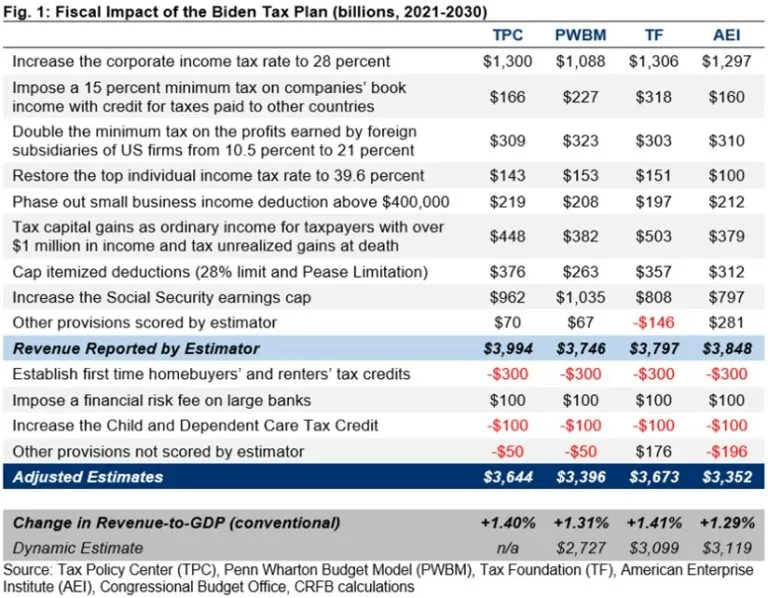

Joe Biden’s economic plan includes raising the corporate tax rate to 28% and increasing taxes on earnings over $400,000. Furthermore, the estate tax exemption would be substantially reduced and Biden has revealed his intention to eliminate the step up in basis for assets at death. If Biden is elected, such a significant tax overhaul would of course require Congressional approval.

Most estimates put the fiscal impact of such measures at around $3.5 trillion over the next decade, with most of the revenue coming from corporations, then income from high earners, followed by social security taxes on high earners. While the prospect of higher taxes arising from a blue wave may cause worry for many investors, the counterbalance for some is that a Democratic sweep would likely result in bigger fiscal stimulus, which could serve to benefit the broader economy. Credit Suisse, for instance, has proposed that a Democratic sweep could actually serve as the most optimal scenario for risk markets. Goldman Sachs has said a Democratic sweep would likely result in the company upgrading its forecasts: “The reason is that it would sharply raise the probability of a fiscal stimulus package of at least $2 trillion shortly after the presidential inauguration on January 20, followed by longer-term spending increases on infrastructure, climate, health care and education that would at least match the likely longer-term tax increases on corporations and upper-income earners.” In recent weeks, President Trump has also been pushing Republicans for “higher numbers” in its stimulus package as he seeks to significantly boost infrastructure spending. For investors, stimulus will be a major point of focus as all potential outcomes are considered.

Could We Have a Disputed Election

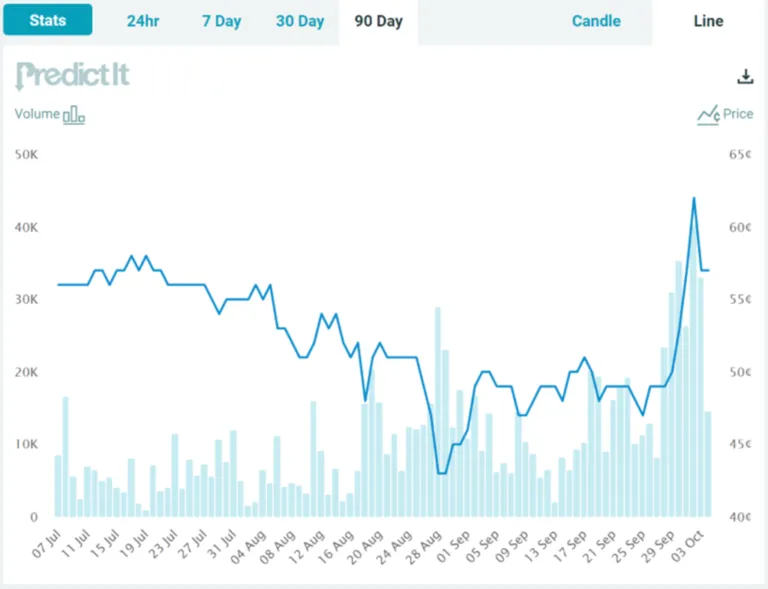

All of this assumes, of course, there is a clear winner. But there are growing concerns that in the event of a close outcome, a disputed result could pose a big risk to the market. The cost of hedging volatility around the election has been increasing in recent weeks and is higher than that of past elections.

Over the last several years, a greater proportion of Americans have voted early, absentee, or by mail (24.9mm in 2004 to 57.2mm in 2016). With 2020’s pandemic, more than 72 million absentee ballots have already been requested or sent to voters across 39 states as less people will be likely to vote in person on Election Day.

There will likely be discussion and debate about how election officials handle absentee/mail-in ballots as voting procedures and controls are largely managed locally across cities and states rather than nationally. This year, the Electoral College is scheduled to meet on December 14, which would be the day by when states would have hopefully finished counting absentee and provisional ballots. There are concerns that a clear election winner may not be decided by then, though, and a disputed presidential election in 2020 would mark the fifth in US history. Looking to the last disputed election as a guide, the S&P 500 plunged nearly 10% in November of 2000 when the presidential election between George W. Bush and Al Gore was held up by a historically tight race in Florida. Some economists believe that other factors were at work, though, given concerns about tech profitability, rising interest rates to combat inflation, and a slowing US economy, and that the disputed election result only accentuated deeper underlying issues at the time.

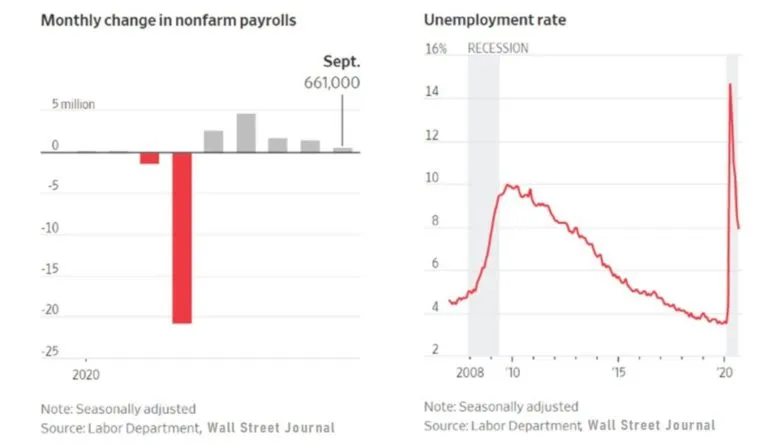

Jobs Are Coming Back But Not Fast Enough

The US has replaced roughly 11 million of the 22 million jobs lost in March and April, with the unemployment rate falling to 7.9% this week from its 14.7% high five months ago.

One concerning trend, however, is the increasing number of furloughed workers now classifying themselves as permanently laid off and unemployed. In April, 88% of workers who recently lost jobs reported their layoffs as temporary (expecting to return to the same role within six months), but in September that figure fell to 51%. Over that same period, the number of people classifying themselves as permanent job losers grew from 2 million to 3.8 million.

Q3 Earnings Expectations

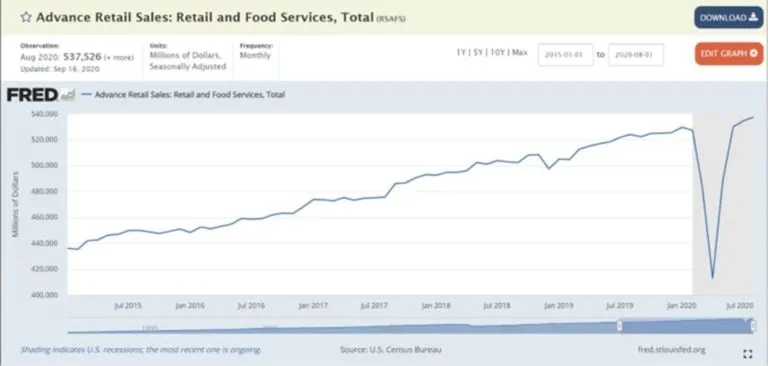

The Q3 earnings season is scheduled to kick off on October 13, with S&P earnings estimated to be down -21.0% from a year ago. This would be an improvement from the –31.9% decline in earnings last quarter. Analysts and companies have actually been revising their estimates higher in recent weeks—the original consensus at the beginning of July was for earnings to decline by -25.4% in the third quarter. The largest earnings estimate increases have been in the consumer discretionary sector. This comes as retail spending in the US has fully recovered and even surpassed pre-pandemic levels.

The Hinge Point: A Vaccine

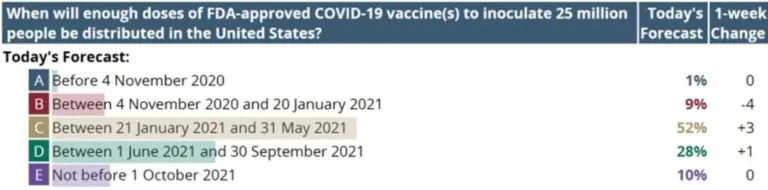

The crux of an economic recovery lies within how soon a reliable vaccine could be made available to the public. The Good Judgment Project, run by professors from the University of Pennsylvania, have employed a team of superforecasters who predict the timing and likelihood of major events around the world. They currently forecast a 10% chance of an FDA-approved COVID-19 vaccine being available to inoculate 25 million people within the US by January 20 next year and a 90% chance of it being available by the end of next September.

While the WHO has said there are 170 vaccine candidates in development with 26 in human trials, there are eight that are close to completing the final phase of testing. According to analysts at Deutsche Bank, the consensus front-runner is the Oxford/AstraZeneca vaccine, with most governments around the world having secured significant quantities. The bank’s economists believe that an available vaccine by mid-2021 would “accelerate the move back out of recession in the second half and secure global growth of around 5.5%.”

Final Thoughts

Our thoughts and prayers are with those individuals and families currently suffering from COVID-19 and dealing with other hardships related to the pandemic. As we enter the final quarter of 2020 and reflect on the challenges faced over the last nine months, we are hopeful that these experiences can widen our perspective and help us grow. Our society has been beset with tribulation before and certainly will confront affliction again. While there are questions that still lie ahead, I would invite you to consider another quote from FDR: “Don’t allow our doubts of today limit our tomorrow.” This dark season shall be but temporary, and will eventually pass, and brighter days lie ahead.