History does not repeat itself, but it does rhyme.

Mark Twain

Have We Seen this Movie Before

In mid-1979, oil prices more than doubled within twelve months. The forces that fed into the dangerous concoction that spawned the Energy Crisis included an exceptionally accommodative Federal Reserve that had kept rates low to combat a previous recession, a global surge in oil demand from a booming world economy, and a geopolitical conflict that drastically reduced oil output.

Last month, brent crude reached as high as $139/bbl, slightly more than doubling the price it traded at a year earlier. Contributing to the swelling oil price has been a global economy eager to bolt out of the pandemic and a Russian invasion that resulted in sanctions on the world’s third largest oil producer.

While on its face, although our current circumstances appear to be a repeat of a world we confronted over forty years ago, when peeling back the layers there are crucial differences that should not be ignored. The unemployment rate stood at 7.2% in 1980 and stagflation was in full effect; GDP growth was negative and the fed funds rate breached 20% by the end of the year as Fed Chair Paul Volcker combated inflation with unprecedented zeal. This stands in stark contrast to a current unemployment rate of 3.6%, with GDP growth expected to be above 3% this year and a fed funds rate that remains close to zero and poised to reach around 2.5% by the end of 2022.

Difficult challenges still lie ahead; with the benefit of past experience, time will tell if we can navigate ourselves to a better outcome in the sequel than the original.

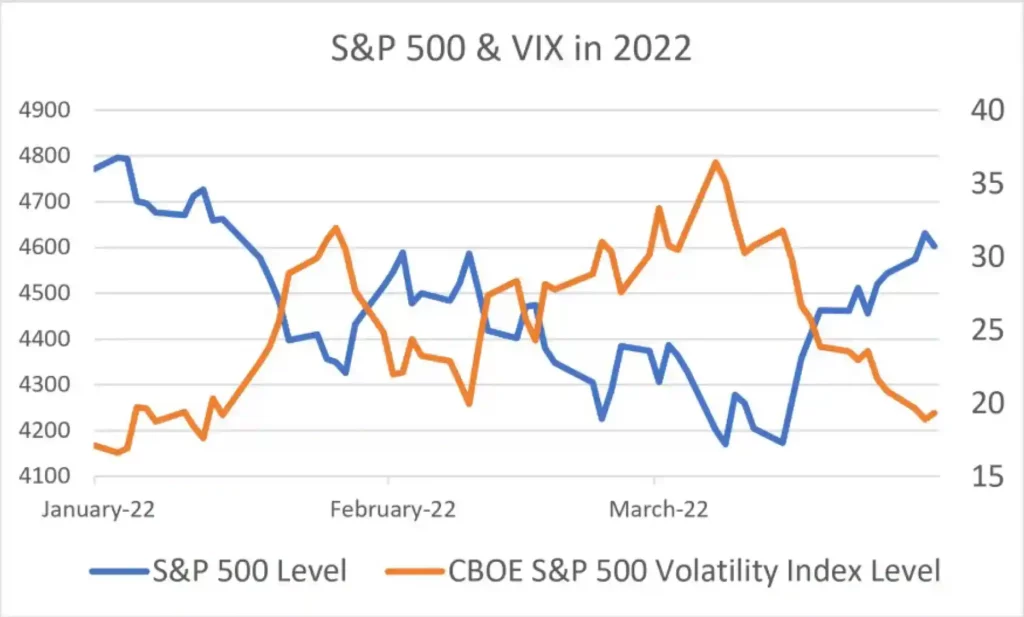

A Bear Market Rally

With the Nasdaq falling into bear market territory on March 14 and the S&P 500 falling as much as 12.5% since the start of the year, stock indexes rallied back hard during the second half of March, even recouping the large majority of the losses incurred during the first quarter of 2022. Meanwhile the Volatility Index also nearly halved over the same period.

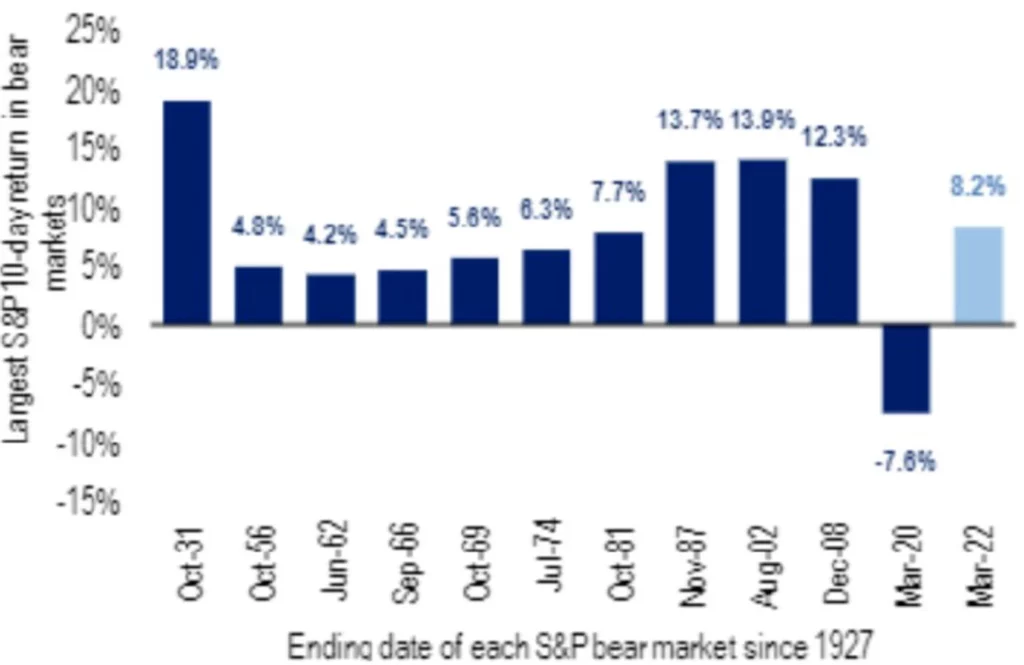

Amidst the backdrop of continued concerns over inflation and fighting in eastern Europe, the sharpness of the rally has prompted a number of market strategists to characterize the rebound as a bear market rally. Strategists from both Morgan Stanley and Bank of America point out that vicious swings to the upside are typical of volatility in bear markets; in fact, some of the S&P 500’s biggest rallies have occurred in the middle of bear markets, and both reports are skeptical of the recent strength and call for investors to sell into the bounce. Bank of America notes that this equity rally surpassed the largest 10-day returns in 7 of the S&P’s 11 bear markets since 1927.

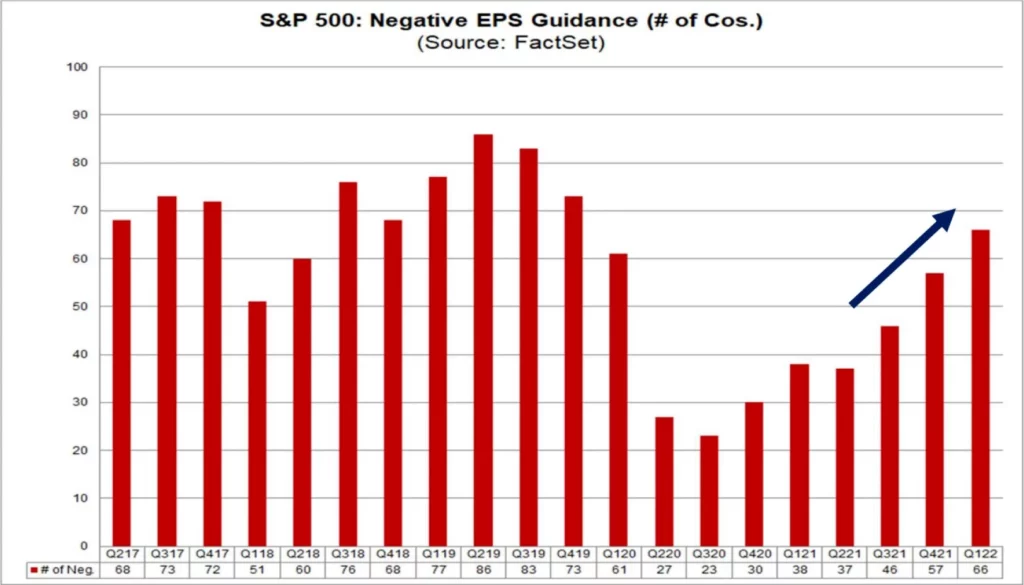

Earnings Outlook Softening

One cause for concern is the dimming outlook on earnings in recent months. At the end of December, analysts forecasted S&P earnings to grow 5.7%. As we approach the end of the quarter, those estimates have been slashed to 4.8%. Furthermore, according to FactSet, 66 companies have issued negative guidance, the third straight quarter that more companies are warning of deteriorating earnings.

Both Goldman Sachs and Morgan Stanley anticipate that companies’ profit margins will be negatively affected by higher wage growth. Goldman’s David J. Kostin said that labor costs dominated the focus of many of the earnings calls last quarter and Morgan Stanley anticipates that pretax profit margins may fall from 17.8% to 10.7%.

Hot Labor Market

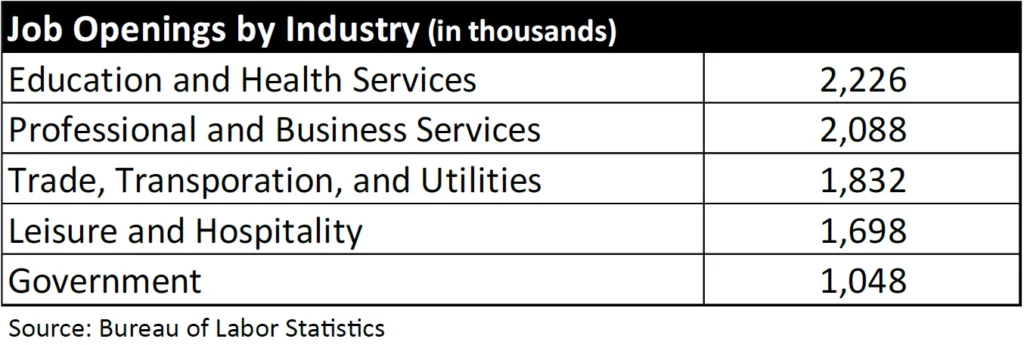

By every measure, the US jobs market is very strong. Unemployment is rapidly approaching the pre-pandemic level of 3.5% and job openings are hovering near all-time highs. Nearly 80% of the job openings at the end of February were in the following areas:

As further evidence of a healthy labor market, Americans are also quitting their jobs at a record pace. With 1.8 job openings available for every person seeking employment, competition for talent will likely remain high. This has also pushed nominal wages up to the fastest level in years. Nevertheless, when adjusted for living costs, though, real wages are actually lower and losing purchasing power.

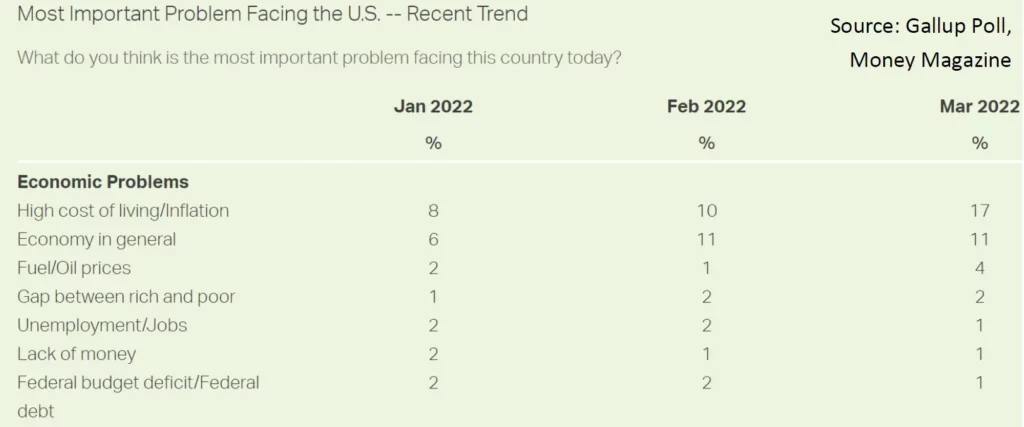

Inflation Has Been Rising Unabated

With prices having risen rapidly throughout 2021, inflation has continued to accelerate higher during the first part of this year. February inflation rose 7.9% from a year ago, the fastest growth since January 1982, marking the sixth straight month that prices rose at an increasing rate. Since the start of the year, Americans have become significantly more concerned about the prospect of facing higher living costs. March’s gallup poll indicates that more than twice as many people now feel that inflation is the country’s top economic concern compared to January.

The First Step in the Journey

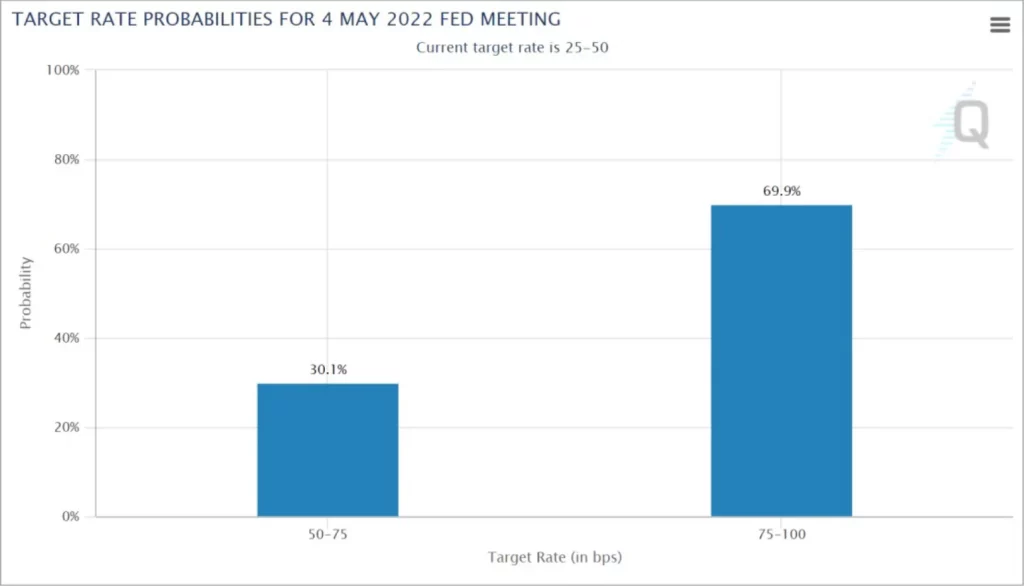

On March 16, the Fed implemented its first rate hike since December 2018 by raising the Fed target 25 basis points. Fed Chairman Jay Powell left the door wide open for a 50 basis point hike at the next May meeting remarking, “We will take necessary steps to ensure a return to price stability… if we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at meeting or meetings, we will do so.” Traders are betting a 50 basis point hike is indeed likely at the beginning of May, pricing in a 70% probability of the target rate jumping 0.5% to a range of 0.75-1.00%.

At this point, the market is pricing in the funds rate to reach the 2.50-2.75% range by the end of this year, 1% higher than where rates traded prior to COVID-19.

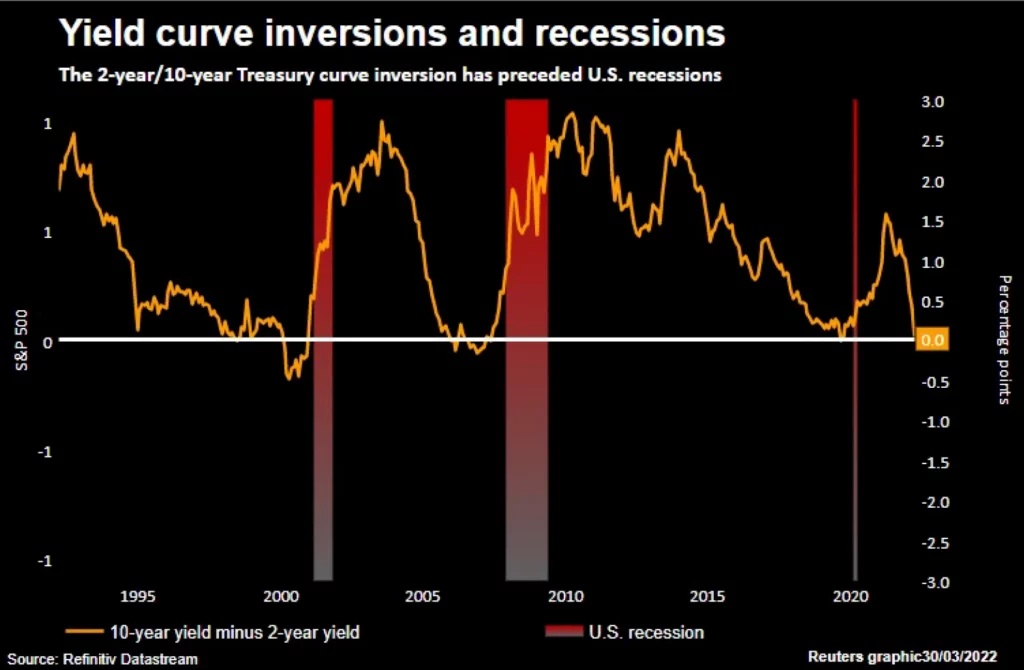

The Yield Curve Has Inverted

The prospect of the Fed pushing up the overnight lending rate has shifted short term yields higher while long term yields have remained suppressed, and parts of the yield curve are becoming inverted. For instance, for the first time since 2006, the 5-year treasury yield went above that of the 30-year by 10 basis points. The more traditional recession indicator, the spread between the 2-year and 10-year yields, went negative on March 31 for the first time since 2019.

Although most inverted yield curves have been accompanied with a recession within 24 months, many market strategists are setting aside conventional wisdom. For those who believe an imminent recession is unlikely, one particular point relates to the Fed’s disproportionate ownership of outstanding US Treasuries that may be artificially keeping long term rates down. Currently, the Fed owns nearly 40% of all outstanding US Treasury bonds; two years ago, their ownership was 23%. There are many who believe the inverted yield curve is primarily a function of the quantitative easing program rather than a reflection of a troubled economy.

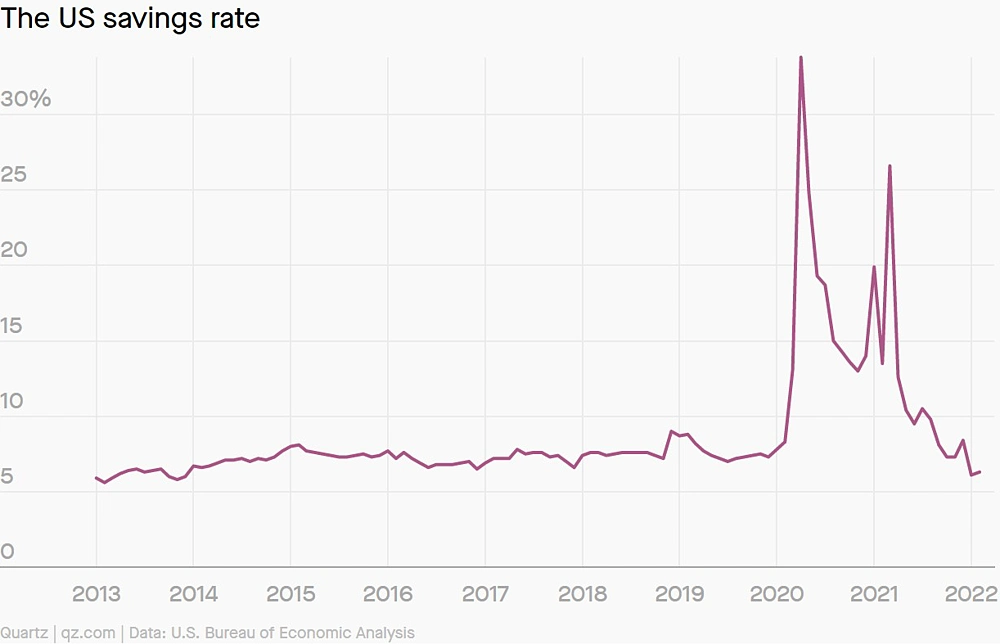

How Long Will the Savings Last?

During the pandemic, households in the US accumulated $2.5 trillion of excess savings and bank commercial deposits ballooned from $13.4 trillion to $18.2 trillion.

This past February, however, households saw their savings rate fall to the lowest level since 2013. With home prices up 18.8% in 2021 and rents up 14% nationally, combined with higher food, energy, and consumer goods prices, households are struggling to put money away. While most families remain in a stronger financial position for now, that is not true of many lower income households. Kathy Bostjancic, chief economist at Oxford Economics, noted, “Consumers overall still have a sizable pandemic-related savings surfeit, however, the lowest quintile households have largely exhausted their savings.”

Will Take Time to Work Through Challenges

The economic, monetary, and geopolitical issues surrounding us, while challenging, are not new. They are similar to those faced more than a generation ago, and arguably less daunting today. Although this story sounds familiar, surprises are inevitable and a quick solution is unlikely; patience and caution is well advised.