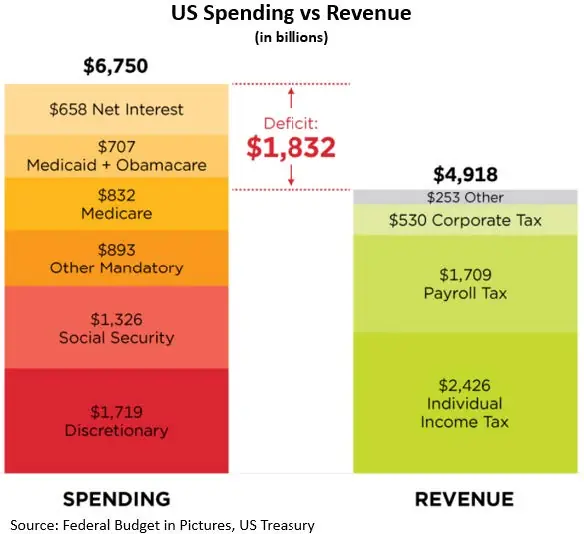

Although concerns related to the United States’ fiscal health are certainly not new, a combination of high interest rates and soaring debt over the past 24 months escalated worries. Last year, the US Federal Government spent $6.75 trillion while collecting just $4.92 trillion in revenue, resulting in a $1.83 trillion shortfall. The current administration campaigned on plans to both reduce spending as well as increase fiscal revenue with the aim of balancing the federal budget, a feat that has eluded the US since 2001.

The Department of Government Efficiency (DOGE), tasked with “modernizing Federal technology and software to maximize governmental efficiency and productivity,” claims to have generated $140 billion in savings as of the end of March. That figure, which cannot be verified, is supposed to include contract and grant cancellations, lease terminations, work reductions, fraud elimination, asset sales, interest savings, and programming/regulatory costs. Numerous analysts and researchers, however, believe the total may be overstated by as much as 5 to 10 times. Others have also pointed to DOGE ignoring lost tax revenue from a smaller IRS and billions of severance dollars paid to laid-off workers. While initially hoping to find savings of $2 trillion to cover the deficit, Elon Musk has now said he is hopeful DOGE can reach $1 trillion in savings. Musk is designated as a “special government employee,” which caps his work at the White House at 130 days. He commented at the end of March, “I think we will accomplish most of the work required to reduce the deficit by a trillion dollars within that time frame.” How he would achieve this feat remains highly unclear, however.

Another pattern the current administration is attempting to break is to bring manufacturing back to the US after decades of shifting production offshore.

By the mid-20th century, the US was the world’s supreme manufacturing powerhouse. During the final three years of World War II, the US provided almost two-thirds of all military equipment to the Allies. In fact, by 1945, more steel was produced in the state of Pennsylvania alone than in Germany and Japan combined. That era has now long disappeared. Many US companies began prioritizing offshoring manufacturing in the 1970s as labor costs and easier regulations could be found abroad. By the turn of the century, American offshoring accelerated, and China overtook the US as the world’s leading manufacturing nation in 2010.

Today, China’s global share of manufacturing output is roughly double that of the US. As a more extreme example, to illustrate China’s current manufacturing dominance, in 2022 China built 1,794 large oceangoing ships compared to five ships built by the US during the same period.

American reshoring came back into focus in 2010 with the formation of the Reshoring Initiative and became a more pressing issue during the Covid-19. The pandemic exposed US companies’ vulnerability to supply chain disruptions and reshoring efforts accelerated. Since 2010, over two million jobs have been brought back to the US.

The current administration is attempting to turbocharge the reindustrialization process by implementing an aggressive tariff strategy aimed at compelling US and international companies to redirect overseas production into America. This will be a challenging process for an economy that has 72% of its economy come from services and just over 10% from manufacturing. Given the US’s large population and relatively high per-capita income, the country’s consumption dwarfs that of other nations.

Due to the enormity of US consumption, tariffs place tremendous pressure on exporters of goods to America. Ordinarily, many could be motivated to seek renegotiating trade terms with the US—either by 1) attempting to persuade the administration to lower US tariffs by reducing their own or 2) retaliate by increasing tariffs on US goods into their own countries. While the response will depend country-by-country, most will likely be disincentivized from raising their own tariffs due to trade imbalances (US has trade deficits with most countries—some exceptions include Hong Kong, Singapore, Australia, UK, Brazil, and the Netherlands) and such action would inflict further harm for both parties.

Their other course of action is to bolster relationships with other trading partners to replace lost sales to the US. Global Trade Alert found that despite the magnitude of US consumption, due to the growth of imports outside of the US, more than 100 economies would likely have fully recovered their lost exports from closure to the US market by 2030 (Mexico and Canada being notable exceptions).